₹10 Crore by 60: The Exact SIP Amount You Need — And Why Every Year You Wait Costs You a Fortune

If you’ve ever wondered what SIP to reach 10 Crore by retirement looks like in real numbers — this article will give you the answer in seconds. And fair warning:

the difference between starting at 20 versus 50 will genuinely shake you.

Let me open with a number that will haunt you if you let it pass.

A 20-year-old investing just ₹5,500 per month will retire at 60 with a ₹10 Crore corpus. That’s less than a Netflix subscription plus two weekend meals. But a 50-year-old? They need ₹2,05,000 every single month to reach the same ₹10 Crore finish line.

Same goal. Same retirement age. A difference of ₹1,99,500 per month.

That’s not a personal finance tip. That’s a life-altering warning.

📌 What You’ll Learn in This Article:

- The Exact SIP Table — Age-by-Age Breakdown

- Why Starting Early is the #1 Financial Decision of Your Life

- If You’re 20: The ₹5,500 Goldmine

- If You’re 30: Still Powerful, But the Clock is Ticking

- If You’re 40: Serious Mode Activated

- If You’re 50: Hard Truths and Real Solutions

- How to Start Your SIP Today in Under 10 Minutes

- FAQs

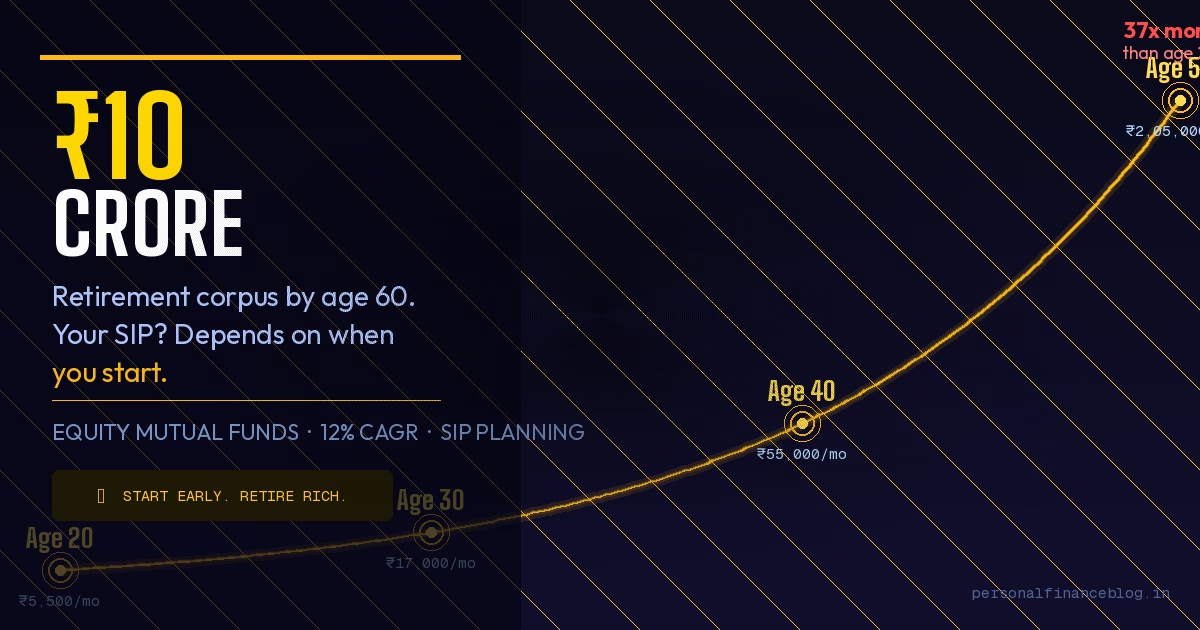

SIP to Reach 10 Crore: The Age-Wise Breakdown

Let’s not bury the lead. Here is the data that every Indian investor needs tattooed on their wall:

| Your Current Age | Monthly SIP Required | Years to Invest | Total Amount Invested |

|---|---|---|---|

| 🟢 20 Years | ₹5,500/month | 40 years | ~₹26.4 Lakhs |

| 🟡 30 Years | ₹17,000/month | 30 years | ~₹61.2 Lakhs |

| 🟠 40 Years | ₹55,000/month | 20 years | ~₹1.32 Crores |

| 🔴 50 Years | ₹2,05,000/month | 10 years | ~₹2.46 Crores |

*Calculations assume an approximate 12% annual CAGR (Conservatives), consistent with historical long-term equity mutual fund returns in India. Past returns do not guarantee future results.

Let that sink in. A 20-year-old invests a total of ₹26.4 Lakhs over their lifetime to get ₹10 Crore. A 50-year-old invests ₹2.46 Crore — and barely makes it. The 20-year-old earns ₹9.73 Crore in returns. The 50-year-old earns only ₹7.54 Crore in returns.

Who works harder? The 50-year-old. Who wins bigger? The 20-year-old — effortlessly.

This is the genius of compound interest. And most people discover it 20 years too late.

Why Starting Early Is the Single Most Important Financial Decision of Your Life

Albert Einstein reportedly called compound interest the “eighth wonder of the world.” Whether he actually said it or not doesn’t matter — because the math is undeniable.

When you start your SIP at 20, your money has 40 years to compound. The growth in the final 10 years alone will likely exceed everything you earned in the first 30 years combined. That’s not poetry — that’s mathematics.

Here’s a way to think about it: Every ₹1 you invest at age 20 is worth approximately ₹93 at age 60 at 12% CAGR. The same ₹1 invested at age 50 is worth only ₹3.1 at age 60.

You’re not just investing money when you’re young. You’re investing time — and time, unlike money, cannot be earned back.

“The best time to plant a tree was 20 years ago. The second best time is now.”

— Ancient Chinese Proverb (that applies perfectly to SIP investing)

🟢 Age 20: The Cheapest SIP to Reach 10 Crore

You need just ₹5,500 per month. Let’s put that in perspective for a moment.

The SIP to reach 10 Crore at age 20 is so low it’s almost unfair — just ₹5,500/month.

That’s less than:

- A mid-range smartphone EMI

- Monthly dining out budget for most urban 20-year-olds

- Two pairs of branded sneakers per year

For most 20-year-olds in India with even a modest salary of ₹20,000–₹30,000, this is absolutely achievable. And yet, most don’t do it. Why? Because at 20, retirement seems like a problem for a much older, much more boring version of yourself.

Here’s the mindset shift you need: You’re not saving for retirement. You’re buying your future freedom.

At ₹5,500/month in a good equity mutual fund SIP, you are on track to never worry about money again. You will retire — if you choose — with a corpus that generates roughly ₹6–8 Lakhs per month in passive income at a conservative 8% withdrawal rate.

That is the power sitting in your hands right now, at age 20, for the cost of skipping a few weekend splurges.

Action Step: Start a ₹5,500 SIP in a diversified large-cap or flexi-cap equity mutual fund today. Set it to auto-debit on salary day. Forget it exists. Thank yourself at 60.

🟡 Age 30: Your SIP to Reach 10 Crore Just Tripled

First, the uncomfortable truth: by waiting until 30 instead of 20, you’ve tripled your required monthly investment — from ₹5,500 to ₹17,000. That one decade of procrastination now costs you an extra ₹11,500 every single month for the next 30 years.

The SIP to reach 10 Crore starting at 30 triples to ₹17,000/month — still very achievable.

That’s ₹41.4 Lakhs extra that you’ll need to contribute from your pocket because you waited.

But here’s the good news: ₹17,000 at 30 is very achievable for most working professionals. By 30, most people are in a career growth phase with rising incomes. If you haven’t started yet, right now — today — is your moment.

The 30-year-old who starts now is still in a far better position than the 40-year-old who procrastinates for another decade. The compounding engine still has 30 years of fuel. That’s more than enough to create life-changing wealth.

A pro tip for 30-year-olds: Use the Step-Up SIP strategy. Start at ₹12,000–₹15,000 and increase by 10-15% every year as your salary grows. You’ll reach ₹10 Crore without it ever feeling like a stretch.

🟠 Age 40: The SIP to Reach 10 Crore Gets Serious

₹55,000 per month. That’s what a 40-year-old needs to reach ₹10 Crore by 60.

I’m not going to sugarcoat this: this is serious money, and it requires serious discipline. For many families at 40, this feels impossible — home loan EMIs, children’s education, ageing parents, lifestyle expenses. The financial pressures of 40 are very real.

But here’s what I want you to consider: What happens at 60 if you don’t start now?

If ₹55,000/month is genuinely not feasible, the answer is not to give up — it’s to recalibrate your goal. Even starting a ₹25,000 SIP now gives you approximately ₹4.5 Crore by 60, which is still a dignified retirement corpus. A ₹35,000 SIP gets you to ₹6.3 Crore.

The worst decision you can make at 40 is to say “I can’t hit ₹10 Crore so why bother.” That thinking has condemned too many people to financial dependence in old age.

At 40, the SIP to reach 10 Crore jumps to ₹55,000/month — a serious but doable target.

Start with what you can. Increase aggressively as loans close and income grows. Use any windfalls — bonus, inheritance, asset sale — to supercharge your corpus with lump-sum investments.

🔴 Age 50: Can You Still Reach 10 Crore? Yes — Here’s How

₹2,05,000 per month. That number looks terrifying. And I’ll be honest with you — for most people at 50, hitting exactly ₹10 Crore by 60 purely through monthly SIP is very difficult.

But before you close this tab in despair, let me tell you what IS possible and what you should actually do:

1. Combine SIP with Lump Sum Investing: At 50, many people have accumulated some savings, FDs, or assets. If you can deploy ₹30–₹50 Lakhs as a lump sum in equity funds today, you dramatically reduce the monthly SIP burden required to reach your target.

2. Revise Your Target: ₹5–7 Crore is still an excellent retirement corpus. A ₹1 Lakh/month SIP for 10 years can get you to approximately ₹5 Crore. That’s not a failure — that’s financial security most Indians never achieve.

3. Delay Retirement by 2–3 Years: Working until 62–63 instead of 60 gives compounding two extra years. At this stage of the curve, those extra years have an outsized impact.

4. Start Immediately — Not Tomorrow: At 50, every single month matters more than at any other age. Each month of delay at 50 costs you more than an entire year of delay cost you at 20. Act today.

The message here isn’t doom — it’s urgency. You have 10 years. That’s 120 months. Make each one count.

How to Start Your SIP in Under 10 Minutes Today

There has never been a time in Indian financial history where starting an SIP was this easy. Here’s your step-by-step:

- Complete Your KYC: If you haven’t done KYC, complete it at CAMS, KFintech, or any mutual fund platform. It takes 10–15 minutes online with your PAN and Aadhaar.

- Choose Your Platform: Reach out to your advisor.

- Select Your Fund Category: For long-term wealth creation (10+ years), a diversified equity fund — either Flexi-Cap, Large & Mid Cap, or Index Fund — is a solid starting point. Consult a SEBI-registered financial advisor for personalised advice.

- Set Your SIP Amount and Date: Choose your salary credit date + 3 days as your SIP date. This ensures money moves before you spend it.

- Automate and Ignore: Set up auto-debit. Do not check your portfolio every week. SIP rewards patience, not obsession.

💡 Pro Tip: The Step-Up SIP Rule

Increase your SIP by 10% every year on your work anniversary. If you start at ₹5,500 at age 20 and increase by just 10% annually, your final corpus could be ₹25–30 Crore — not ₹10 Crore. That’s the power of combining SIP growth with income growth.

The Most Expensive Mistake in Personal Finance Is Waiting

I’ve spent 20 years writing about money. I’ve interviewed hundreds of wealthy individuals and hundreds of people who struggled financially in retirement. And the single common thread I’ve found is this:

The wealthy ones didn’t earn more. They started earlier.

Whether you start today or a decade from now, knowing your SIP to reach 10 Crore gives you a clear, actionable target — and a reason to start immediately.

The person reading this at 20 has a superpower that no amount of money can buy later in life — time. The person reading this at 50 has urgency, and urgency is its own form of fuel.

Wherever you are on this spectrum, the right move is identical: Start today. Start now. Start with whatever you have.

Ten years from now, you will look back at this moment and either thank yourself or regret yourself. The only variable is what you do in the next 10 minutes.

Open your mutual fund app. Set up that SIP. Your 60-year-old self is watching.

Frequently Asked Questions

What rate of return is assumed in the ₹10 Crore SIP calculation?

These calculations are based on an approximate 12% annual CAGR, which is broadly in line with the long-term historical returns of diversified equity mutual funds in India. However, actual returns will vary based on market conditions, fund selection, and timing. Past performance does not guarantee future results.

Is ₹10 Crore enough for retirement in India?

At a conservative 7–8% withdrawal rate, ₹10 Crore can generate approximately ₹5.8–6.6 Lakhs per month in passive income. For most Indian households, this provides a highly comfortable retirement. However, inflation and lifestyle requirements vary, so consider consulting a certified financial planner to determine your personal target.

Which mutual fund is best to start a SIP for ₹10 Crore goal?

For long-term goals of 20–40 years, diversified equity funds such as Flexi-Cap Funds, Large & Mid Cap Funds, or Nifty 50 Index Funds are widely recommended by financial advisors. Always choose funds based on your risk profile, investment horizon, and financial goals, ideally with guidance from a SEBI-registered investment advisor.

Can I start a SIP with less than the recommended amount?

Absolutely. Starting with even ₹500–₹1,000/month is better than not starting at all. You can increase your SIP amount over time using the Step-Up SIP feature available on most platforms. The key principle is: start small, start now, grow over time.

What is Step-Up SIP and should I use it?

A Step-Up SIP (also called Top-Up SIP) allows you to automatically increase your SIP amount by a fixed percentage or amount every year. Given that incomes typically grow over time, a 10–15% annual step-up is both achievable and dramatically improves your end corpus. It’s one of the most powerful features in mutual fund investing and highly recommended.